Mutual funds and its types

When talking about Which Mutual Fund to invest in, we mentioned that we’ll talk more about the types of funds available in a separate article. This is the one. We often invest in mutual funds, without knowing the different types of funds available to us, and what purposes they serve! In this article, let’s talk about these variants and how we should decide on which one to choose.

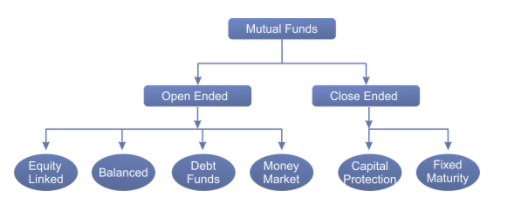

While you see a dozen types of funds when you go to the investing screen on your chosen platforms, broadly, there are only three categories of funds – Equity, Debt, and Hybrid funds. Like the names suggest, equity funds invest a majority of the money you put into stocks directly – meaning they’re more at risk and can also earn a higher return, debt funds choose bonds and debt instruments which give a lower return but have relatively lower risk, and hybrid funds are a combination of equity and debt. Lets delve into each of these categories and see the different sub-types within them. Try finding which type your chosen fund belongs to, and think about why you chose that particular fund to invest in?

Equity – These make up most of the options available to us as investors. By changing the sectors invested in, or the percentage invested in different classes of equities, by investing in different markets, or investing in indices directly, equity funds allow you to invest in the markets through an expert fund manager. This, for most of us, is a better alternative than investing in stocks directly. Stocks may seem attractive and there are a zillion advisories which send us messages promising us returns similar to what what Nigerian Princes send us in emails. But stocks are an expert’s domain. It needs close monitoring of fundamentals and technicals and require an in-depth knowledge gained over time. It is a fact that most of those who get into the markets without this knowledge will lose their money sooner or later. While it is rewarding to get that knowledge and work out a portfolio by ourselves, it is also a fact that most of us will not be able to do it. Take the safer route – get an equity fund and leave it to the experts. The returns may be tempered when compared to stocks directly, but atleast we won’t lose the shirts on our backs! Blue Chip, Large Cap, Mid Cap, and Small Cap funds are the most visible equity funds. There are various sectoral funds as well – like Banking and Financial services fund (which only invests in companies pertaining to that sector), Healthcare fund, IT fund, and so on. If you wish to invest in a particular sector, those funds may be a better alternate to buying the different stocks you’d like, since they’re spread out. Blue Chip funds invest only in the top companies in our stock markets. Large cap companies are those with a market capitalisation of over ₹20000 crores. Mid cap is between ₹5000 crores to ₹20000 crores, and Small cap is under ₹5000 crores. Funds titled large cap / mid cap / small cap would choose companies which pertain only to the respective capitalisation standards. A sub-class of equity funds are tax savings funds or ELSS funds. These have a lock in period of atleast 3 years and give us tax savings of upto ~₹45000.

Debt – Debt funds are safer alternatives and typically earn a couple of percentage points higher than a fixed deposit. Like with equity funds, there are various permutations and combinations in debt funds too. Many of them have a percentage of their total assets under management in government or corporate bonds. Depending on the aggressiveness of the fund, that percentage is tweaked. Investing in higher risk debt instruments may show up a higher return % but with that comes a higher risk. Almost all debt funds have a portion of their funds in the money market – which is to make them liquid and earn FD-like interest rates. That money is used as a hedge and is deployed when opportunities arise – like when RBI cuts rates etc. Sometimes we see debt funds also earn blockbuster results. That would almost exclusively be because of a bond they were holding skyrocketing because of market movement. Or a special situation that the fund manager made use of and exited with healthy profits. The safest of these funds are GILT – which invest exclusively in government paper. The Indian government gives out various kinds of bonds and investing opportunities, and sometimes even those give 10-12% if the interest rate in the markets goes the other way. These bond rates are typically inversely proportional to the RBI’s repo rates. While investing in a debt fund, temper your expectations to around 2-3% more than an FD. If you’re looking at getting a higher return percentage but would like to keep away from full-equity funds, choose hybrid funds.

Hybrid Funds – For most people, these funds make a lot of sense. Since many of us don’t take an investment profile test while getting started in mutual funds, we don’t really know our risk appetite. And most of us end up with an aggressive equity fund since those are the ones which show up on top when you search funds based on past performance. When the markets fall, those fall hard too. Ofcourse they recoup quickly also, but many investors book losses fearing further falls. That is the story of a majority of people in the markets – whether through stocks or through funds. Hybrid funds allow us to choose an instrument which is made up of both equity and debt. The fund managers have a ratio they work with. Say 60 equity, 40 debt; or vice versa. Based on market movements and predictions, the manager keeps moving funds back and forth, thereby reducing exposure and risk to the investor. Sometimes they may want to invest upto 80-85% in equity or conversely reduce it to 50%. In market situations like at the beginning of Covid-19, many hybrid fund managers would have sold off equity and moved it into debt. And when the markets fell heavily, they would have bought some of it back. This flexibility is often missing with 100% equity funds, since it is imperative for them to keep maximum cash deployed in the markets. Like you probably understand by now, hybrid funds will earn a tad lower than equity funds and probably a bit higher than debt funds.

The reason a mutual fund makes sense for many of us when compared to stocks directly, is because of the flexibility and hedging options it gives us. If one doesn’t choose a fund according to the goals we have in mind, it defeats the purpose of choosing a mutual fund. If you have questions about types of funds or anything you read about on this blog, do reach out to us via any of our Social Media accounts – Twitter, Facebook, Quora.