Which mutual fund should I invest in?

This post is a part of an ongoing series on answering common queries on Mutual Funds. You can look up the other posts in the series here.

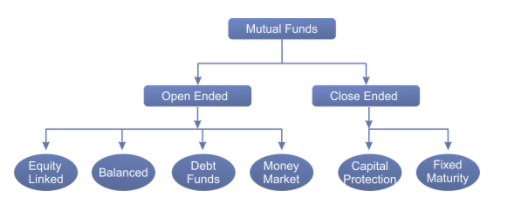

There are several categories of funds that are available for us to invest into. When you look at moneycontrol or economictimes, or check the best-performing funds on your investment platform, you’ll notice Debt, Equity, Hybrid, Fund of funds, Gilt, ETFs etc as options to choose from. There’s a post we wrote about each of these mutual funds and its types. That’ll make for interesting reading. If you’re aware of the types, let’s get into this article and answer a more fundamental question – why so many options and who should choose these?

Before you get investing, it is important that you check your investment profile. What do you aspire to do with this investment, what is your horizon, what is your risk appetite? Most investment platforms and financial websites get you to answer a few questions and give you a fair answer – whether you’re an aggressive investor, moderate, or conservative. Take that quiz from a couple of places first. Google ‘check my investment risk profile’, and head over to a couple of sites you trust. In a few minutes you’ll have an idea. Most platforms even tell you what mix of funds will work best for your profile. Don’t get investing yet, let’s understand this better.

The typical investor sorts funds based on last one or three year performances and judges that a parcitular fund is better than the others. That’s a rather rudimentary method of investing. A particular fund may have a stock which gave bumper returns in one year and that’ll show up on top; but that performance will seldom repeat in the coming years. That is the key reason why many portfolios don’t match the market. Pose these questions to yourself – are you a short term investor or do you want to build a corpus for the future? Or you probably want to generate wealth and leave it to your kids? What returns are you happy with? Don’t say 25% per year! That’s not practical. Compare mutual funds against fixed deposits, which are currently earning about 5-6% per year. If we say we’re happy with 9-10%, that’s a good starting point. You decide what you want – 15% is an accepted answer also, but the risk appetite needs to be quite high then. For short term investing, you don’t want to get into a volatile fund – especially if you know that you’ll need that money someday soon. Choose a hybrid fund which keeps adjusting the money invested between equity and debt funds. That way, you’re hedged to a certain level. Of course you won’t make as much as a pure equity fund, but you won’t lose big either. If you’re investing for the very long term, an ETF may make more sense than an actual mutual fund. Read up about them on our post about ETFs – What is an Exchange traded fund?

If you’re moving money out from your fixed deposit into a mutual fund, you probably want a safer bet than pure equity. Then a debt fund or a GILT fund (which only invests in government bonds and securities) may make more sense. They are much more conservative than equity funds. If you have a horizon of atleast 3 years, and you want a more aggressive approach, get into an ELSS (Equity Linked Savings Scheme) which has a lock-in for 3 years but also gives you a tax benefit of about ₹44000. Make the most of what the government allows us to save – if you have unused limit under section 80C. A whole different approach is if you’re buying when the market has fallen significantly. Like in the first months of Covid when Nifty fell from 12000+ to under 8000 points. If you were deploying funds in such a time, you wouldn’t want to go for a debt fund and minimise your possible yield. Since the risk would be much lower then, you would put in more of your money into a pure equity fund. If you were a moderate investor, you would still choose equity but probably a blue-chip fund. Now, if you were choosing to invest via an SIP, then all of this over-thinking can pretty much be ignored. The purpose of an SIP is so that you don’t have to do all this research! Enter anytime, but for the first couple of years, whenever the market falls by atleast 10% or so, add in extra capital so you lock in lower NAVs. Then the SIP can steadily grow. But you’ll also want to keep taking out money when it has grown significantly to book profits. No mutual fund is a lifetime investment product. When the market falls, your funds will fall drastically too. Set a benchmark – say 25% growth. Once that is achieved, you may want to take out 25% of your funds (or more or less, depending on the need you have), but keep the SIP going till you retire.

Lastly, don’t have too many funds in your basket. That’s another typical amateur mistake. Choose a max of 3-4 funds spread across different categories. Choosing multiple funds in the same segment won’t make sense since they will probably have an overlap of stocks. Also, stay away from thematic or sectoral funds unless you do your research diligently and keep tabs on the sector. If you have specific questions, feel free to reach out to us via our social media handles – Twitter, Facebook, Quora.