Who should I listen to?

This is one of the most fundamental questions we have when we think of investing! We don’t really want to spend time to learn and understand our investment profile and set goals for our investments. Instead, we want someone to answer this question for us, and we keep asking tips and advice from everyone we meet. Once the urge to ask for investment tips gets into our brain, it is like a bee in the bonnet, and is extremely difficult to get rid of! And here is a fact – someone else’s tips will never work for you in the long term. Period. Invest in this policy, take that mutual fund, this stock will make you a millionaire, buy that bond, invest in an upcoming country, whatever advice people give you when you ask this question, is often gleaned from someone else! Seldom do we see people who do their own research dole out advice, because they know that a particular decision is correct ONLY based on the circumstances and thought process of the investor. How will they be the same for them and for you?

Enough generalisation. Lets get a bit specific. I was listening to this brilliant podcast by Nithin Kamath of Zerodha. The guy is remarkable! He makes a point that struck home bigtime – if we want to buy a refrigerator, we will do oodles of research. If someone recommends a particular brand and model, we will not just go and buy it directly. Instead, we’ll run comparisons, see options, and then decide. For a refrigerator (or any product for that matter), we do a ton of research. But when it comes to investing our life’s hard-earned savings, we just take advice at face value and put it into whatever someone tells us? How silly is that?? Mushrooming of ‘advisory’ companies in India is a direct outcome of this weird thought process we’ve somehow developed. It is a fact that most of these companies are not advisories at all. That should actually be obvious listening to the ridiculous chaps calling us daily, and the half-baked company names they call us from. These companies just pick up advice from all popular banks and advisors, and recycle it to their gullible subscribers. Often, they recommend small-cap companies which they get a cut on, and it is a dirty game, but they’re all raking in money! All because we don’t want to do research ourselves but are willing to bet big money on the ‘advice’ of some chaps we don’t know and will never actually meet.

The same is true for distributors of investment products. Not all of them are bad. If you trust your banker and if you have a premium account with them, you may actually get good advice. But those are in the minority. 90% of the calls, mails, and messages we get from our banks or any platform we invest via are for products we never asked them for, right? How is this a ‘recommendation’? It is just cold-selling, in the hope that someone will buy. Many people often do, as the literature is worded like a sales pitch and is based on the simple fact that most people reading that prospectus will never actually spend time comparing the product with their goals.

When we go to a doctor, we pay him for his time. We trust his judgment because he is dispensing his knowledge after listening to us. The same holds true for lawyers, fashion designers, interior decorators, and most professionals who trade their time for money. But when it comes to investment, we just take advice from people who we are not paying. Read that again – we are not paying any of the professionals or agencies we take this advice from. The fly-by-the-night sms advisory firms don’t count. An investment agency or a professional should know you and your goals as well as your doctor or lawyer does. They are professionals too – if you are serious about it. Advanced markets like the United States have most of their serious investing done through paid financial advisors. These people either take a cut on the profits or have a flat fee. Most hedge funds actually started off as portfolio management systems and then grew into funds as they built trust of investors. In India also, we have a lot of excellent portfolio management services. But again, don’t go rushing into what you think is good based on Google reviews 🤦🏻♂️. You should know your advisor or agency. It is a personal rapport. They should ask you questions about what is your investment horizon, what kind of financial goals you have, what is the purpose behind each product you are looking at, and so on. That is because we often don’t ask ourselves these questions. Once that is done, they should be invested in your success and monitor it on a continuous basis.

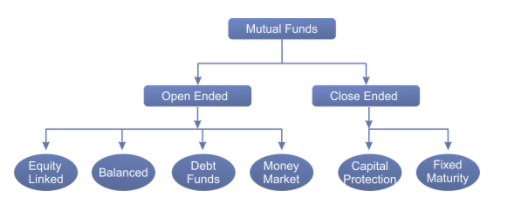

We wrote a post about Where to buy Mutual Funds online. In that, we made this point about direct mutual fund platforms being the best choice if your bank isn’t giving you informed advice anyway. The same holds true for stocks. If you’re not getting proper management, just head over to a low-cost brokerage. No sense paying big money if it isn’t worth it. Insurance too – online policies usually have better terms, and they aren’t available offline. The money you save on all of these products will add up to some serious numbers as this is a long-term decision. Considering that, what you’ll pay an advisor is actually much lower. That is, if you are serious about investing, and if your corpus is large enough to warrant that decision. If you’re just starting out in the markets or if the numbers you’re thinking are still small, just go with an Exchange Traded Fund – you usually can’t go wrong with it if you have atleast a few years as investment horizon. If you have a specific query, feel free to reach out to us via any of our Social Media platforms – Twitter, Facebook, Quora.